What Happens After You File: A Look Inside Our Tax Review Process

- Steven C. Balch, CFP®

- May 5

- 4 min read

Tax season wrapped up last month, which means we are officially in tax review season for all our clients.

Here’s what we review with clients and why we do this twice a year.

Spring Review: After Tax Season

The Tax Return Review

Right after-tax season, we ask clients to share their completed tax returns with us.

Your tax return tells us a lot about where things stand and where we need to focus for the year ahead. We use it for three main purposes.

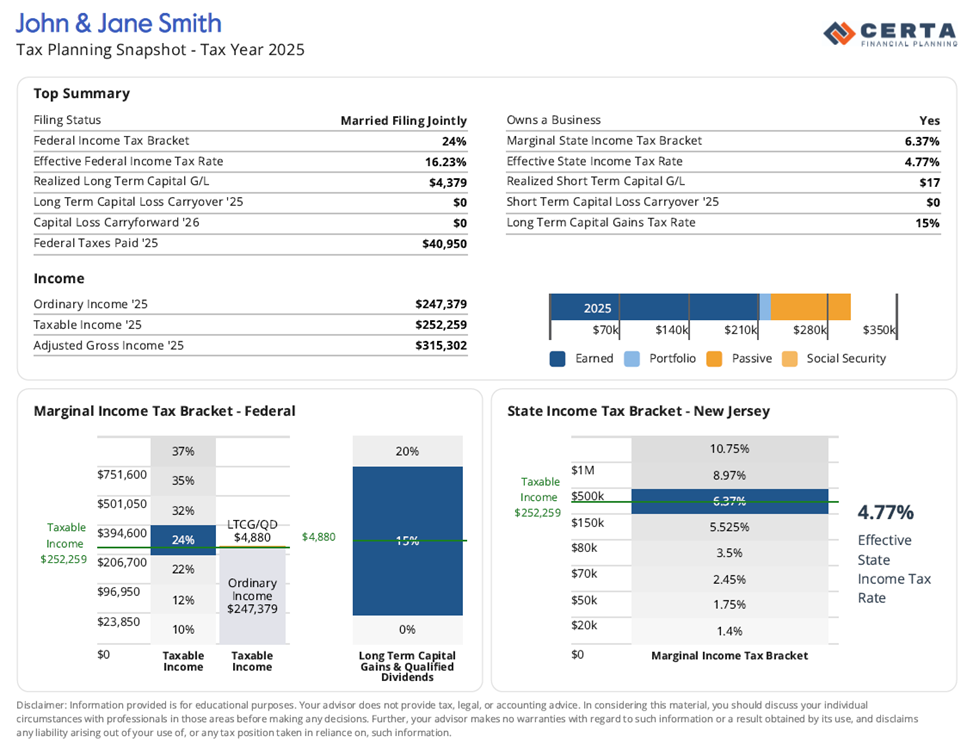

Purpose 1: Build your tax snapshot

The first thing we do is pull together what we call a tax snapshot. This is a simple, clear summary of your tax picture. The report tells us your total income, your effective federal and state tax rates, and the key numbers and thresholds that matter for your situation. It becomes our baseline for the year.

The below charts are shown for illustrative purposes only. Individual situations will vary. Consult your tax professional and/or legal expert about your individual tax situation before making any decisions

Knowing where you fall relative to important thresholds like Medicare IRMAA brackets, capital gain rates, or Roth conversion opportunities allows, us to make better decisions throughout the year instead of guessing.

Purpose 2: Catch mistakes

Tax returns can have errors. Sometimes it’s a minor oversight. Sometimes it’s a costly one.

Over the years, we’ve caught things like:

Property tax deductions missing or applied incorrectly

RSUs being taxed twice due to incorrect cost basis

Missing or misreported 1099 income

Unexpected income from sales or distributions

Retirement contributions not properly recorded

And many other mistakes

We’re not your CPA, but we do act as a second set of eyes.

Catching something in May is a lot easier than catching it the following April.

Purpose 3: Set the game plan for this year

This is the most important part. Once we understand last year’s tax picture, we can plan for this one.

What we’re looking at depends on where you are:

If you’re still working, we look at:

Whether your withholdings are on track

Upcoming bonuses, RSUs, or income spikes

Whether to adjust pre-tax vs. Roth contributions

Deferred compensation decisions

If you’re retired or near retirement, we focus on:

How much income you can take while staying in a favorable tax bracket

Whether Roth conversions make sense this year

Managing around IRMAA thresholds

How to structure withdrawals across accounts

This is where tax planning becomes proactive, not reactive.

Fall Review: Before Year-End

The Year-End Check-In

By fall, most of the year’s income picture has come into focus. We have enough data to see whether the plan we set in the spring is still on track or whether we need to make some adjustments before December 31. Once January arrives, most of the levers are gone.

What we review in the fall

We gather recent pay stubs, updated projections, and any new information that’s come up since the spring. Then we run through a set of questions depending on your situation:

If you’re still working:

Are you on track to meet safe harbor and avoid penalties?

Has income come in higher or lower than expected and do we need to adjust estimated payments for January?

Is this a lower-income year where we can take advantage of Roth conversions or capital gains?

Does a Roth IRA or backdoor Roth contribution make sense?

For business owners: where does income stand, are estimated payments correct and what should go into the retirement plan before December 31?

If you’re retired:

Have we optimized the tax bracket or is there room to do more before year-end?

Are we on track for IRMAA thresholds, or do we need to pull back on income?

Is there a Roth conversion opportunity that still makes sense at this income level?

Are there positions in the portfolio with losses or gains we should harvest before December 31?

Should we adjust withdrawals before year-end?

Have RMDs been handled correctly?

Why This is Part of How We Work

Managing money, especially for high earners and retirees, means looking at the whole picture.

The spring review tells us where you’ve been and sets the direction for the year. The fall review makes sure we’re still on track and captures any last-minute opportunities before the year closes. Together, they help us invest your money in a way that’s not just focused on returns but focused on what you actually keep after taxes.

Good tax planning starts once your tax return is done, or before, if you file an extension. Then it continues through the year and wraps up at year-end. If you work with us, this kind of yearly tax planning isn’t optional. It can be effective to protect and grow your wealth.

- Steve Balch, CFP®

When You’re Ready to Take the Next Step, Here’s How I Can Help You:

Work with me. If you’re a high-income earner or retiree and want to learn how we help people like you retire confidently and take control of your financial life, click here to schedule a call with me.

Ask me a financial question. If there’s something you’ve been wondering about financially - taxes, investments, retirement, or anything else - send me a message on LinkedIn. I’m happy to discuss and help you find clarity.

Download my free eBook — How to Reduce Your Lifetime Tax Bill. This guide is filled with actionable tax-planning strategies to help high-income earners and retirees keep more of what they’ve worked hard for. You’ll learn practical ways to minimize taxes, optimize withdrawals, and build a smarter, more efficient retirement plan. Download here.

Comments