Strategies for Navigating a Potential Lost Decade

- Steven C. Balch, CFP®

- Apr 9, 2025

- 3 min read

Goldman Sachs recently made headlines by predicting that the S&P 500 will return 3% yearly for the next decade, significantly below the long-term average of around 10%. Additionally, other firms, like JP Morgan and Vanguard, have been sounding the alarm and warning investors about potential muted returns in the US stock market over the coming years. Understandably, headlines like these may concern many investors about how their portfolios may be impacted.

Lost decades are not new for the S&P 500. The first lost decade was in the 1970s as the stock market struggled through the oil crisis of 1973-1974, a severe recession, and persistently high inflation. Between December 1969 and December 1979, the S&P 500 index saw negligible growth. The second lost decade was more recent, being bookended by the bursting of the dot-com bubble and the financial crisis of 2007-2008. From January 2000 through December 2009, investors in the S&P 500 saw a negative total return. The good news is that both of these lost decades resulted in compressed valuations, leading to significant market outperformance over the following 10+ years.

In light of these historical lessons, if we are to see a third lost decade, it is paramount for investors to have a plan and stick to it. Here are some strategies for navigating a potential Lost Decade:

1. Diversify Your Investments: Spreading investments across various asset classes—such as stocks, bonds, and real estate—can mitigate risk. By diversifying, one can reduce the impact of a downturn in any single sector or market on their overall portfolio. Even when the S&P 500 provided a negative return to start the 2000s, many diversified investors still saw positive returns as other asset classes like commodities, REITs, bonds, and International equities helped to counter the poor US market performance.

2. Diversify Your Strategies: Every account does not have to have the same risk tolerance. Compartmentalizing your accounts and having a strategy with a timeline for each helps you stay the course. An easy way to do this is with a Bucket Plan Strategy. Your now bucket should have your emergency funds to cover 6-12+ months of expenses. Your soon and mid-term buckets can comprise CDs, intermediate-term fixed income, and maybe some lower volatile equities positions, depending on your risk tolerance. Your last bucket, the long-term bucket, is your most aggressive allocation and has the longest time horizon. Using your now, soon, and mid-term buckets to cover needs during volatile markets allows you to let your long-term bucket recover.

3. Have a Plan: Investing without a plan is like building IKEA furniture without reading the directions. You end up frustrated and potentially making irrational decisions. Having a financial plan can help you better understand your risk tolerance and the portfolio return you need to reach your financial goals. Additionally, your plan can be re-evaluated to see how lower-than-expected returns impact the success of reaching your goals. The financial plan is the blueprint for your investment strategy and the foundation for your peace of mind.

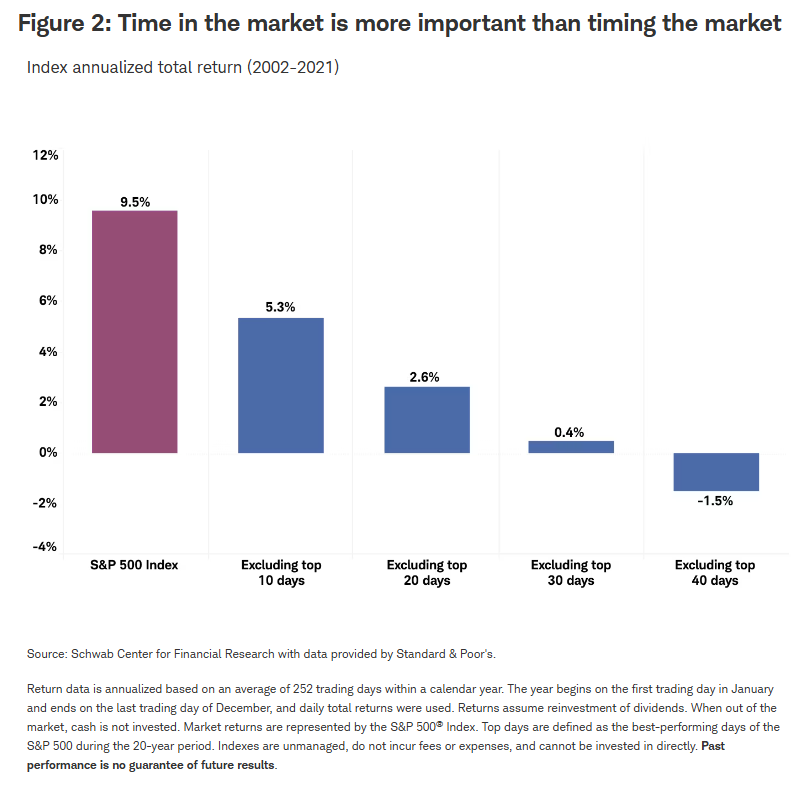

4. Keep Investing: For those not in retirement, continue to save and add to your long-term investment accounts. Accumulating assets at lower prices can be beneficial when the markets eventually turn positive. For those in retirement, remember your buckets and stay the course. The long-term assets will be needed later on to keep up with inflation.

5. Maintain a Long-Term Perspective: While lost decades can be daunting, historical data suggests that markets tend to recover over time. Adopting a long-term investment horizon and maintaining patience can be crucial to weathering periods of instability.

If you are unsure if your plan and portfolio are prepared for a potential lost decade in the US markets, please schedule a call with me to discuss further.

Comments