How to Turn Your Retirement Savings Into a Paycheck

- Steven C. Balch, CFP®

- 2 days ago

- 3 min read

For most of your working life, a paycheck arrived consistently and the goal was straightforward: save a portion, invest it, and let it grow. In retirement, that dynamic reverses completely. The paycheck turns off and now the money you built has to support you, potentially for 25 or 30 years.

Most people have never been shown how to make that transition effectively. This is what we call the Paycheck Replacement Plan, and this is how we customize it for each client.

Start With What You Need

Many people approach retirement planning by looking at their portfolio balance first.

A better approach is to start with your spending.

What does it cost to live the retirement you want?

Let's assume you need $150,000 per year to support your lifestyle.

The next step is identifying your guaranteed income sources. For most retirees, that means Social Security and sometimes a pension.

In this example:

Social Security (Spouse 1): $50,000

Social Security (Spouse 2): $30,000

Total Guaranteed Income: $80,000

If your spending need is $150,000 and guaranteed income covers $80,000, your portfolio needs to provide the remaining $70,000 per year.

That's your income gap.

Instead of wondering whether your portfolio is "big enough," you now have a clear target. Your investments need to generate approximately $5,800 per month to support your retirement lifestyle.

Structuring Your Portfolio for your Paycheck

Once you know the gap, the next step is organizing your portfolio to fill it reliably without forcing you to sell investments at the wrong time.

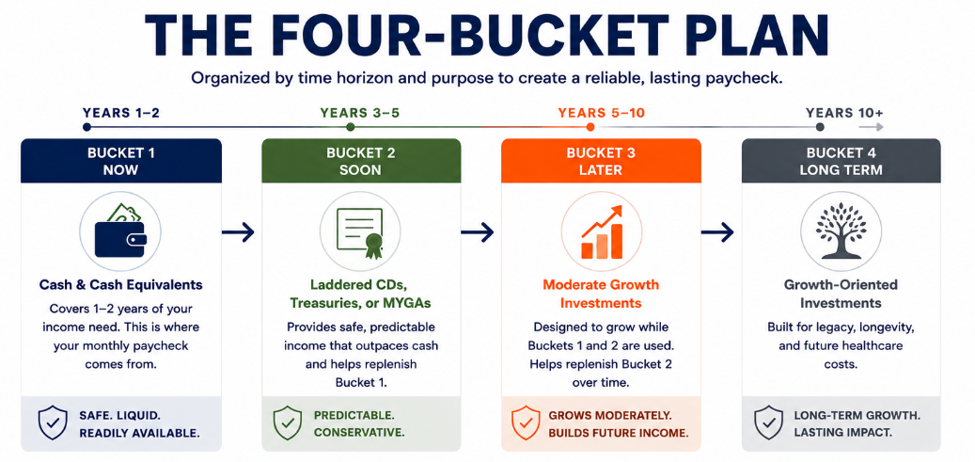

We use a four-bucket approach that separates your money by purpose and time horizon. Each bucket plays a specific role, and together they create a self-replenishing income system.

Bucket 1: Now

This bucket holds one to two years of spending needs in cash and cash equivalents. In this example, that is roughly $70,000 to $140,000.

This is where your retirement paycheck comes from each month.

Because this money isn't exposed to stock market volatility, your near-term spending remains protected regardless of what the markets are doing.

Bucket 2: Soon

The second bucket covers years three through five. This may include laddered CDs, Treasury securities, or other conservative investments designed to provide stability and predictable returns.

As Bucket 1 is spent down, Bucket 2 becomes the next source of replenishment.

Bucket 3: Later

This bucket is invested with a five-to-ten-year time horizon.

Because this money won't be needed immediately, it has time to weather market volatility and pursue moderate growth.

By the time this money is needed, it has had years to grow and work for you while the first two buckets were covering expenses.

Bucket 4: Long-Term

The final bucket is designed for the future. This portion of the portfolio focuses on long-term growth and may help fund later retirement years, healthcare expenses, inflation, and legacy goals.

Because this money may not be touched for a decade or more, it has the longest runway to grow.

Putting It Together: Your Paycheck Replacement Plan

This is how we help clients make the transition from saving for retirement to living in retirement. Not with a generic withdrawal rule or a one-size-fits-all strategy, but with a personalized income plan built around their lifestyle, goals, and financial picture.

We identify your income gap and then structure your portfolio with the goal of generating reliable income while giving your long-term investments the time they need to grow.

The result is more than just a monthly paycheck. It's the confidence to spend, travel, give, and enjoy retirement without constantly worrying about the next market headline.

Our Paycheck Replacement Plan is designed to help you replace your paycheck with purpose, protect your financial independence, and enjoy the freedom you've worked so hard to achieve

- Steve Balch, CFP®

When You’re Ready to Take the Next Step, Here’s How I Can Help You:

Work with me. If you’re a high-income earner or retiree and want to learn how we help people like you retire confidently and take control of your financial life: click here to schedule a call with me.

Ask me a financial question. If there’s something you’ve been wondering about financially - taxes, investments, retirement, or anything else - send me a message on LinkedIn. I’m happy to discuss and help you find clarity.

Download my free eBook — How to Reduce Your Lifetime Tax Bill. This guide is filled with actionable tax-planning strategies to help high-income earners and retirees keep more of what they’ve worked hard for. You’ll learn practical ways to minimize taxes, optimize withdrawals, and build a smarter, more efficient retirement plan. Download here.

Comments